For the full calendar year of 2025, the Standard & Poor’s 500 Index advanced 16.4%, the Dow Jones Industrial Average gained 13.0% and the Nasdaq Composite grew 20.4%. It almost felt like two completely different years, as the equity market experienced two distinctly different phases: one pretty negative and one very positive. On February 19th, the S&P 500 closed at its third all-time high of the year, gaining 4.5% year-to-date. By March, the S&P had given up its gains for the year, but the negative phase had barely begun. On April 2nd, President Trump announced “Liberation Day”, and spelled-out his intention of using an aggressive tariff policy to restructure the global economy. The administration’s “reciprocal tariff rates” were multiples of what the markets were expecting. By April 7th, the market had surrendered 21.0% off its high of February. After a slight dead cat bounce, the S&P was down 15.0% by April 8th. Bearish sentiment was rampant. The bullish phase of 2025 started on April 9th, when the Trump administration announced a 90-day pause for tariff negotiations, and a 10% temporary tariff rate for most trading partners. The market bounced up almost 10% on the day. By the end of June, the S&P 500 Index had surged 22%, marking a new all-time high. To quote Ferris Bueller, “Life comes at you fast.”

Tariffs were most certainly the main factor in the market’s tumultuous behavior in 2025. In 2026, we expect to see more uncertainty tied to the administration’s favorite negotiating tool. As a reminder, the ability of the Executive to institute tariffs under the International Emergency Economic Powers Act (IEEPA) is being considered by the Supreme Court as we write this. The Court of International Trade (a U.S. court, despite its name) already ruled against the administration. The appeal, now being considered by the Supreme Court, gets to the major question of what is an acceptable and proper delegation of authority to the Executive Branch by the Legislative Branch. We expect that the administration will lose its appeal, and we are puzzled as to why the Supreme Court seems to be dragging its feet on a ruling. It is an important decision that will have long-ranging consequences for this administration and future administrations, both inside and outside of trade disputes.

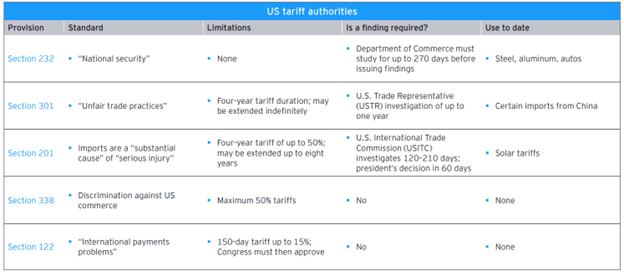

In case of an adverse ruling, the Trump Administration has been preparing alternative avenues to implement tariffs, or continue implementing the tariffs already announced. Most of the other authorities envisioned are disadvantaged relative to the IEEPA, having mandatory hearings, discovery investigations, time limits or tariff limitations. The following table prepared by Ernst & Young summarizes the authorities and their limitations.

If the Administration’s IEEPA tariff authority is ruled unconstitutional, it raises the question of whether the $224 billion of tariffs already collected will have to be refunded and whether trade deals already agreed to, under the threat of onerous tariffs, are valid. We expect litigation and uncertainty. If tariffs are removed, it would be moderately disinflationary for the Consumer Price Index, we believe.

Besides tariffs, the other elephant in the room in 2026 is Artificial Intelligence (AI). In early 2025, AI stocks had tariff-like indigestion when a small Chinese AI company released a highly-performing model with an accompanying scientific paper that claimed the model’s performance was achieved with older GPU chips. AI stocks dropped 30% on average, as the market began to countenance the economics behind the massive spending of the largest hyperscalers. Heretofore, Wall Street was enamored of the rapid capability growth of the leading AI models, and, perhaps selfishly, captivated by the amount that the hyperscalers were spending and committed to spend. Wall Street is never disinterested.

DeepSeek, the Chinese AI company, claimed to create an impressive AI model on a budget that was a fraction of the size that was being used to create other leading models. Even more troubling, DeepSeek was not even a subsidized Chinese government-supported champion, but rather a subsidiary of an obscure private Chinese hedge fund. People started to question about when the hyperscalers would achieve profitability on their investments, and whether money was being misspent. Indeed, the perception of value of cutting-edge Nvidia GPUs and Google TEUs was being called to account. Nvidia lost 17% of its stock value, or almost $600 million of market capitalization in one day. The reaction was violent, but short-lived.

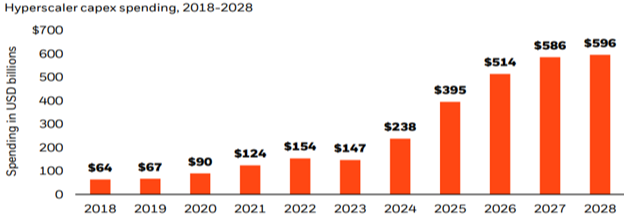

The following chart shows the actual capital expenditures and committed expenditures of Amazon, Meta, Alphabet, Microsoft and Oracle:

DeepSeek has released seven more AI models updates since its first market-shaking model. Although most showed incremental improvements, the major AI labs released better models, including OpenAI’s GPT-5, Anthropic’s Claude Opus 4.5 and Google’s Gemini 3. Additionally, the hyperscalers continued to commit to large and increasing capital expenditures, suggesting that they believed that the most advanced frontier models still needed the most advanced chips to succeed. Finally, Nvidia reported that its new and improved chips were sold-out for the foreseeable future, and that the spot values of its older generation second-hand chips were increasing. These votes of confidence reversed the AI market’s temporary identity crisis.

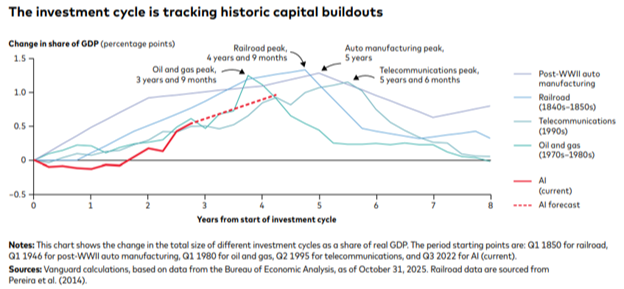

It is instructive to compare the current AI Infrastructure capital intensity with other historical large-scale investment periods:

The above chart looks at the capital intensity of AI (capital expenditures as a % of GDP) with post-WWII manufacturing (1946), Telecommunications (1995), Petroleum (1980) and Railroads (1850). The conclusion is that AI Infrastructure investment as a percentage of GDP is trending in a similar arc as the previous large-scale build-outs, and might reach its peak 4-5 years after its 2022-23 inception point. It doesn’t take much imagination to conclude that the adoption at scale of AI will be transformative for the economy. The same could be said about the adoption at scale of the railroads, electricity and the internet. All were transformative, and all left some early leaders in financial straits or bankrupt. As venture capitalist Jerry Neumann writes, “Anyone who invests in the new new thing must answer two questions: First, how much value will this innovation create? And second, who will capture it?” (https://colossus.com/article/ai-will-not-make-you-rich/ ; we will post Jerry’s cranky and illuminating essay on our website.) Mr. Neumann suggests that the real winners from new and transformative infrastructure are not very obvious in the early innings. We think about the implications of that quite a lot.

The country has too much debt. The geopolitical trading system is being changed in real time, and is subject to unpredictable internal and external influences. Inflation is stubbornly high. The current Federal Reserve is at war with the current Administration. Stock market valuations are high and credit spreads are low. The jobs market is sluggish and consumer expectations are near all-time lows. The U.S. Dollar Index lost 9.4% of its value last year, the largest loss since 2017. Judging from the market reactions after the DeepSeek announcement and the tariff tantrum, investors are a bit skittish. Yet, against this wall of worry, the S&P 500 recorded its third annual double-digit gain. Do not discount the good news: the Fed is in an easing cycle; new tax rates offer some payors relief; regulatory abatement should aid many corporations and entrepreneurs; and corporate fundamentals are good. Companies in the S&P recorded record profit margins last year (+12%) and their net cash flow neared $4.0 trillion, over $1.0 trillion more than the pre-pandemic baseline. Given the superior stock market performance of the last three years, it is time to revisit portfolio allocations, asset allocation and diversification levels. Call us. We can help.